Small Modular Reactors: An Executive Intelligence Report on Commercial Readiness, Infrastructure Investment and Global Deployment (2026–2035)

- Green Fuel Journal

- 4 days ago

- 22 min read

Three small modular reactor projects in the United States — TerraPower, X-energy and Kairos Power — moved from demonstration to construction under a US$3.2 billion federal cost-sharing programme confirmed on 23 June 2026, marking the sector's clearest transition yet from research category to commercial infrastructure.

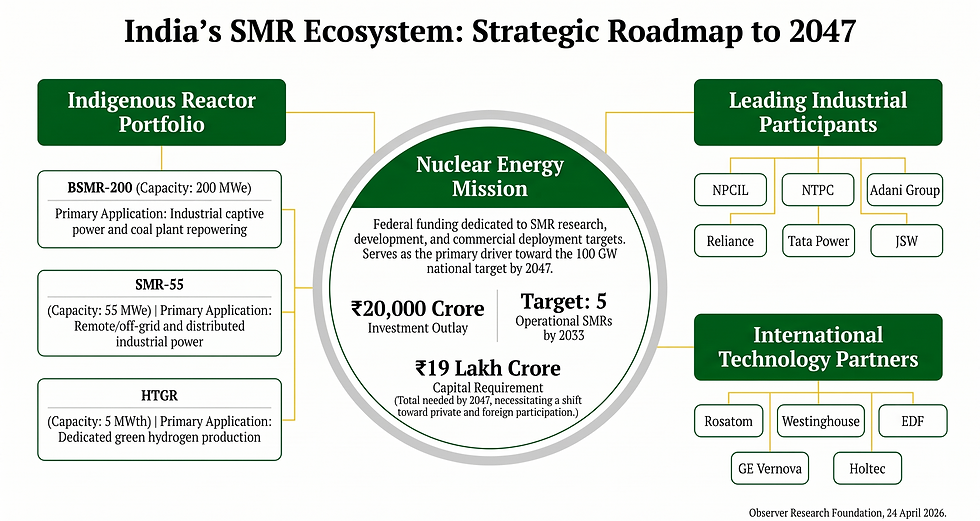

India has matched this momentum with a ₹20,000 crore Nuclear Energy Mission, launched in the 2025 Union Budget, targeting five indigenously developed small modular reactors operational by 2033 as a step toward 100 GW of nuclear capacity by 2047.

This report evaluates small modular reactors as an infrastructure asset class — benchmarking commercial readiness, capital requirements, regulatory maturity and industrial demand globally, with a dedicated assessment of India's distinct strategic position through 2035.

The International Energy Agency states that small modular reactors could become a major driver of nuclear growth in advanced economies, provided projects are delivered on schedule and costs fall through standardised manufacturing.

The International Atomic Energy Agency attributes accelerating global interest to small modular reactors' ability to supply flexible, low-carbon electricity, industrial heat and hydrogen at materially lower upfront capital requirements than conventional large reactors.

This report draws exclusively on verified institutional, governmental and market data to assess where small modular reactors stand today and where capital is most likely to flow through 2035.

Executive Intelligence Synthesis

Why are Small Modular Reactors strategically important in 2026?

Small modular reactors moved from demonstration technology to investable infrastructure in 2026 as three United States developers entered construction under federal cost-sharing, Sweden approved its first national reactor financing package, and India committed ₹20,000 crore to indigenous deployment. Rising electricity demand from AI data centres, industrial decarbonisation targets and energy security pressure are the three forces converting government interest into funded, under-construction projects across multiple jurisdictions simultaneously.

Five strategic signals define the small modular reactor landscape entering the second half of 2026.

Signal 1 — Small modular reactors have entered commercial construction. On 23 June 2026, the United States Department of Energy confirmed that three Advanced Reactor Demonstration Program projects — Kairos Power, TerraPower and X-energy — have moved into construction, the first concrete transition of advanced reactor designs from demonstration to commercial build-out under a US$3.2 billion federal cost-sharing programme spanning seven years.

Signal 2 — Government financing has shifted from research grants to project-stage capital. Sweden approved its first financing package for new nuclear reactors on 25 June 2026, selecting Rolls-Royce SMR technology, while the United Kingdom committed nearly £600 million in public financing for Rolls-Royce SMR through Great British Energy – Nuclear in April 2026.

Signal 3 — AI data centre electricity demand is a primary driver of renewed nuclear investment. The convergence of artificial intelligence power demand with the requirement for firm, low-carbon baseload electricity is cited across institutional sources as central to small modular reactors' relevance to industrial and digital infrastructure planning.

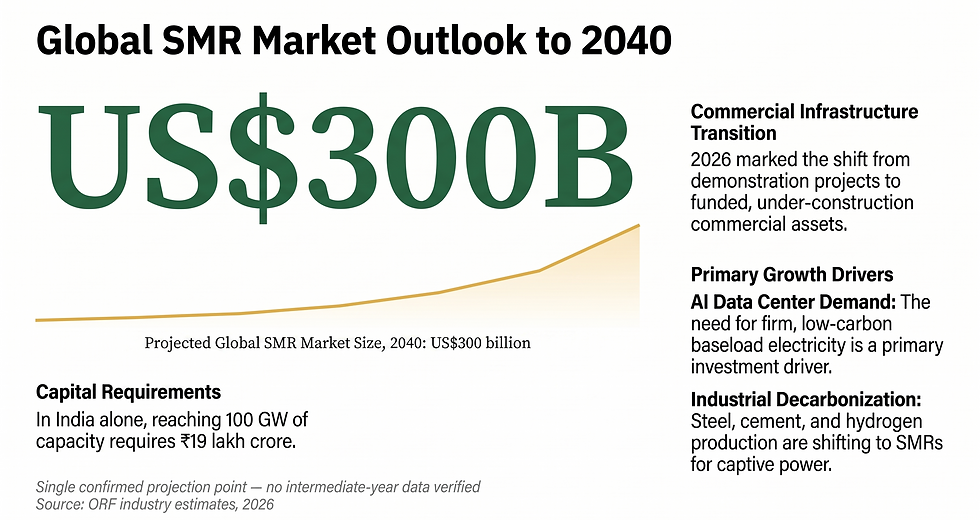

Signal 4 — India has become a significant future SMR market. India's installed nuclear capacity stands at approximately 8.78 GW, representing only 3.1% of national electricity generation, against a stated target of 100 GW by 2047. The Observer Research Foundation estimates this expansion will require approximately ₹19 lakh crore in investment — a scale that cannot be met through public funding alone and that is now opening to private and potentially foreign capital.

Signal 5 — Infrastructure investment opportunities extend beyond reactor construction. The European Commission's first dedicated SMR Strategy, adopted in March 2026, projects 17–53 GW of European SMR capacity by 2050 and targets supply-chain development, regulatory sandboxes and coordinated licensing — confirming that capital opportunity spans fuel supply, grid integration, manufacturing and engineering, procurement and construction (EPC) capacity, not reactor vendors alone.

GFJ Intelligence Note: The shift from demonstration to construction-stage financing across the United States, Sweden, the United Kingdom and the European Union within a single twelve-month window is the clearest evidence yet that small modular reactors have moved from research category to commercial infrastructure asset class.

Macro Context & Strategic Drivers

Why are governments investing in Small Modular Reactors?

Governments are investing in small modular reactors because they offer firm, low-carbon power that complements variable renewable generation and reduce construction risk through factory-based modular manufacturing compared with large conventional reactors. The combination of gas price volatility, energy security pressure, industrial decarbonisation targets and rising data centre electricity demand has converted policy interest into direct capital commitments across the United States, Sweden, the United Kingdom and the European Union in 2026.

Net Zero commitments and gas price volatility are driving renewed nuclear investment.

Net Zero commitments across major economies require firm low-carbon generation that can run independently of weather conditions — a role renewables alone cannot fill at the pace required. Geopolitical energy security concerns, sharpened by recurring gas price volatility, have pushed governments toward domestically controllable baseload sources.

The International Atomic Energy Agency frames this combination — decarbonisation, baseload reliability and energy security — as the foundation of renewed nuclear interest globally, with small modular reactors positioned as the segment best able to respond quickly given shorter construction timelines than gigawatt-scale plants.

Why SMRs Are Different

Factory manufacturing of standardised modules — rather than bespoke on-site construction — is the central economic argument for small modular reactors: it converts construction risk into manufacturing risk, which is more predictable and scalable. Modular deployment allows capacity to be added incrementally, reducing the up-front capital exposure that has historically deterred investment in large nuclear projects.

The International Energy Agency's The Path to a New Era for Nuclear Energy assessment states explicitly that small modular reactors could become a major driver of nuclear growth in advanced economies, conditional on projects being delivered on time and on costs falling through standardisation — meaning the investment case depends on execution discipline, not technology alone.

Investment Watch: The first-of-a-kind cost premium remains the central unresolved variable in the small modular reactor investment case. Until multiple units are manufactured at scale, reported project costs — including TerraPower's approximately US$4 billion Natrium project — should be read as early-stage benchmarks rather than representative fleet economics.

Finland's Steady Energy is piloting Europe's first small nuclear district-heating reactor.

Small modular reactor applications are expanding beyond grid electricity into industrial heat, hydrogen production and district heating. Finland's Steady Energy launched a pilot project in February 2026 for what is described as Europe's first small nuclear district-heating reactor, demonstrating that small modular reactor demand is no longer limited to power generation alone.

High-temperature reactor designs are also being developed specifically for hydrogen production, and AI data centre operators are emerging as a distinct procurement category given their requirement for reliable, low-carbon, always-on electricity.

India-Specific Analysis

What is India's strategy for Small Modular Reactors?

India's strategy centres on the Nuclear Energy Mission, launched with a ₹20,000 crore outlay in the 2025 Union Budget, targeting five indigenously developed small modular reactors operational by 2033 as a step toward 100 GW of nuclear capacity by 2047. The programme combines indigenous reactor designs — BSMR-200 and SMR-55 — with legal reforms opening the sector to private and potentially foreign participation, targeting industrial captive power, coal plant repowering and green hydrogen production.

India's Nuclear Energy Mission

India's nuclear sector enters this transition from a modest base: approximately 8.78 GW of installed nuclear capacity, accounting for just 3.1% of national electricity generation, against a government target of 100 GW by 2047 — more than an elevenfold increase.

The Nuclear Energy Mission, announced by Finance Minister Nirmala Sitharaman in the Union Budget on 3 February 2025, allocates ₹20,000 crore specifically to small modular reactor research and development, with a stated target of five indigenously developed units operational by 2033.

The Finance Minister stated separately that development of at least 100 GW of nuclear energy by 2047 is essential for India's energy transition, directly tying the small modular reactor programme to the country's broader energy security and industrial competitiveness agenda.

"A Nuclear Energy Mission for research and development of Small Modular Reactors (SMRs) will be set up with an outlay of ₹20,000 crore. At least five indigenously developed SMRs will be operational by 2033."— Nirmala Sitharaman, Finance Minister, Government of India, Union Budget speech, 3 February 2025 (Press Information Bureau

Bharat Small Modular Reactor Programme

The Department of Atomic Energy and the Bhabha Atomic Research Centre are advancing three principal indigenous reactor designs. The BSMR-200, a 200 MWe reactor, and the SMR-55, a 55 MWe design, form the core of the near-term commercial pipeline, alongside a High-Temperature Gas-Cooled Reactor of up to 5 MWth intended specifically for hydrogen production.

These designs are being developed for captive industrial power, repurposing of retired coal-fired plants, supply to remote and off-grid regions, hydrogen production and industrial decarbonisation, rather than as standalone utility-scale generation assets.

Reactor Design | Capacity | Primary Application |

BSMR-200 | 200 MWe | Industrial captive power, coal plant repowering |

SMR-55 | 55 MWe | Remote/off-grid applications, distributed industrial power |

High-Temperature Gas-Cooled Reactor | Up to 5 MWth | Green hydrogen production |

NPCIL is targeting a 5 GW Bharat Small Modular Reactor capacity build-out by 2047, embedding the indigenous programme directly within the national 100 GW target rather than treating it as a separate technology track.

Regulatory Reform

India's ability to mobilise the estimated ₹19 lakh crore required to reach the 100 GW target depends on legal reforms currently underway: amendments to the Atomic Energy Act and to the Civil Liability for Nuclear Damage Act, both intended to open nuclear generation to private participation and enable foreign investment under controlled ownership structures.

On 1 February 2025, the government's budget proposals confirmed an intention to open the historically state-controlled nuclear sector to private firms. As of mid-2026, detailed implementation rules for these reforms remain in development — the regulatory transition, not the technology, is the principal near-term constraint on private capital deployment.

India Perspective: India's nuclear capacity must grow more than elevenfold — from 8.78 GW to 100 GW — within roughly two decades. At an estimated ₹19 lakh crore investment requirement, this is unachievable through public capital alone, making the pace of Atomic Energy Act and Civil Liability Act reform the single most important variable for investors assessing India SMR exposure.

India's Industrial Opportunity

Government and policy institutions have identified steel plants, cement plants, aluminium manufacturing, data centres, green hydrogen production, coal plant repowering and remote industrial clusters as the principal industrial applications for Bharat Small Modular Reactors.

This sector-specific framing distinguishes India's approach from utility-scale grid deployment models seen elsewhere: small modular reactors are positioned primarily as captive industrial power and decarbonisation infrastructure for hard-to-abate sectors rather than conventional grid generation assets.

NTPC, Nuclear Power Corporation of India Limited, Adani Group, Reliance Industries, Tata Power and JSW Group are the Indian industrial participants reported to be exploring the emerging market. On 24 June 2026, Adani Group Chairman Gautam Adani confirmed the conglomerate's entry into the sector through Adani Atomic Energy, with the company targeting 10 GW of nuclear power capacity by 2035.

"Our entry into nuclear energy through Adani Atomic Energy is another confident step towards securing India's long-term energy future."— Gautam Adani, Chairman, Adani Group, Annual General Meeting, 24 June 2026 (Reuters)

Rosatom, Westinghouse Electric Company, Électricité de France, GE Vernova and Holtec International are the international technology partners reported to be in discussion for India's nuclear expansion — indicating that India's domestic reactor programme is likely to be complemented by international technology licensing arrangements rather than pursued on a purely indigenous basis.

Operational & Technical Deep Dive

How do Small Modular Reactors work and where are they most useful?

Small modular reactors are factory-fabricated nuclear units, typically below 300 MWe, transported to site for installation rather than built piece-by-piece in place — converting much of the construction process into standardised manufacturing. This reduces capital risk relative to large reactors and makes them commercially attractive for industrial captive power, hydrogen production, district heating and AI data centre electricity supply, where reliability and deployment speed matter as much as scale.

How Small Modular Reactors Work

Major reactor components are fabricated in a factory setting under controlled, repeatable conditions, then transported to the project site for installation — the defining commercial feature of small modular reactors. This differs fundamentally from large conventional reactors, where most construction occurs on-site over many years and is exposed to project-specific delays, labour availability and weather risk. Factory fabrication is the basis of the cost-reduction thesis underpinning the sector: as production volume rises, learning-curve effects are expected to reduce unit costs in a way that has historically proven difficult to achieve in bespoke, large-scale nuclear construction.

Major Reactor Technologies

TerraPower's Natrium design, under construction in Wyoming, is a 345 MW sodium fast reactor. X-energy's Xe-100 design, planned for deployment in Texas, is a high-temperature gas-cooled reactor, with four 80 MW units planned by 2030. Kairos Power's Hermes Demonstration Reactor in Tennessee uses molten salt technology. India's own programme spans pressurised-water-derived designs (BSMR-200, SMR-55) and a dedicated high-temperature gas-cooled reactor for hydrogen production.

No single reactor technology dominates the global pipeline; commercial readiness is currently most advanced for sodium fast and high-temperature gas reactor concepts moving through United States federal demonstration programmes.

Technology | Representative Project | Status |

Sodium Fast Reactor | TerraPower Natrium, Wyoming | Under construction |

High-Temperature Gas-Cooled Reactor | X-energy Xe-100, Texas | Under construction; 4 units targeted by 2030 |

Molten Salt Reactor | Kairos Power Hermes, Tennessee | Construction underway (2026) |

Indigenous PWR-derived | BSMR-200 / SMR-55, India | Development stage under Nuclear Energy Mission |

Commercial Readiness Assessment

At least 68 active small modular reactor designs exist worldwide, yet only 2 commercial small modular reactor plants are currently operating — both in Russia and China, according to International Atomic Energy Agency design tracking summarised by the Observer Research Foundation.

This gap between design proliferation and operational deployment is the clearest available measure of where the sector stands: technology diversity is high, but commercial proof points remain scarce. The transition of three United States projects into construction in June 2026 represents the most significant recent narrowing of that gap.

Key Statistic: Of at least 68 active small modular reactor designs tracked globally, only 2 are currently operating commercially — both in Russia and China. Commercial readiness, not design innovation, remains the binding constraint on the sector.

AI data centre power is the most discussed emerging demand driver for Small Modular Reactors.

AI data centres require firm, low-carbon, always-on electricity, positioning them as a distinct demand category for small modular reactors beyond grid supply. Hydrogen production is supported by high-temperature reactor designs, including India's dedicated 5 MWth unit. District heating is being piloted in Finland by Steady Energy. Industrial captive power for steel, cement, aluminium and chemicals — explicitly identified in India's industrial opportunity framework — and remote or off-grid community power represent further distinct demand pools, each with different procurement structures and risk profiles.

Named Company Case Studies

Which companies are leading the commercial race for Small Modular Reactors?

The companies furthest advanced toward commercial deployment are the three United States developers now under construction with federal cost-sharing support — TerraPower, X-energy and Kairos Power — alongside India's state-led NPCIL Bharat Small Modular Reactor programme and Sweden's government-financed selection of Rolls-Royce SMR technology. Construction status and confirmed government financing, rather than design announcements alone, are the clearest current differentiators of commercial credibility.

NPCIL & Bharat Small Modular Reactor (India)

NPCIL, operating under India's Nuclear Energy Mission, is targeting 5 GW of Bharat Small Modular Reactor capacity by 2047, anchored by the BSMR-200 and SMR-55 designs and supported by the ₹20,000 crore research and development allocation. The programme's commercial roadmap is tied to coal plant repowering, captive industrial power and hydrogen production rather than open grid competition.

With private-sector entrants such as Adani Group now committing to 10 GW of nuclear capacity by 2035, NPCIL's role is likely to evolve from sole developer toward technology anchor within a broadening industrial ecosystem, contingent on the pace of Atomic Energy Act and Civil Liability Act reform.

TerraPower

TerraPower's Natrium reactor — a 345 MW sodium fast reactor under construction in Wyoming at an estimated cost of approximately US$4 billion — is among the most commercially advanced small modular reactor projects globally. The project is supported by United States Department of Energy funding under the Advanced Reactor Demonstration Program and was confirmed by the DOE on 23 June 2026 to have entered the construction phase. TerraPower's deployment probability is assessed as high relative to global peers given its confirmed construction status and federal cost-sharing.

X-energy

X-energy's Xe-100 high-temperature gas-cooled reactor programme, targeting deployment in Texas, plans four 80 MW reactors by 2030. Like TerraPower, X-energy was confirmed by the Department of Energy on 23 June 2026 to have entered construction under the Advanced Reactor Demonstration Program, supported by federal cost-sharing under the broader US$3.2 billion programme.

Kairos Power

Kairos Power's Hermes Demonstration Reactor in Tennessee, using molten salt technology, is also confirmed under construction as of June 2026 under the Advanced Reactor Demonstration Program. As a demonstration-stage project, Kairos Power's near-term role is establishing licensing and operational precedent for molten salt designs — a technology category with comparatively less global construction experience than sodium fast or high-temperature gas reactors — making its commercialisation pathway somewhat longer than TerraPower's or X-energy's, despite shared federal backing.

Rolls-Royce SMR holds the strongest confirmed European government financing to date.

Rolls-Royce SMR was selected by Sweden for its first nuclear financing package on 25 June 2026 and is backed by close to £600 million in United Kingdom public financing through Great British Energy – Nuclear as of April 2026. Sweden's developer, Blykalla, signed a cooperation agreement with Hitachi Energy on 29 June 2026 to integrate grid infrastructure for future deployment.

GE Vernova, Holtec International and Rosatom are reported to be engaged in international technology discussions, including with India, though specific commercial project data for these developers was not available in verified research for this report and is therefore not detailed further here.

Developer | Project / Design | Verified Commercial Status |

TerraPower | Natrium, Wyoming (345 MW) | Under construction; ~US$4bn |

X-energy | Xe-100, Texas (4 × 80 MW) | Under construction; targeted 2030 |

Kairos Power | Hermes, Tennessee | Construction underway, 2026 |

NPCIL | BSMR programme, India | Development stage; 5 GW by 2047 target |

Rolls-Royce SMR | UK / Sweden deployment | Government-financed: ~£600m (UK); selected by Sweden 2026 |

Executive Insight: Confirmed government cost-sharing — not design novelty — is the most reliable signal of near-term commercial readiness across the current small modular reactor developer landscape.

Friction, Risk & Systemic Bottlenecks

What are the biggest risks facing Small Modular Reactor deployment?

The principal risks facing small modular reactor deployment are high first-of-a-kind capital costs before serial manufacturing reduces unit prices, licensing frameworks designed for conventional large reactors rather than modular designs, constrained commercial supply of High-Assay Low-Enriched Uranium (HALEU) fuel, and — particularly in India — a private financing gap against an estimated ₹19 lakh crore capital requirement that public funding alone cannot meet.

Capital Cost Challenges

The International Energy Agency and Observer Research Foundation both identify high capital cost as the foremost barrier to small modular reactor scale-up: early projects face first-of-a-kind cost overruns that will only be resolved once serial manufacturing establishes a genuine learning curve.

TerraPower's approximately US$4 billion Natrium project, for a 345 MW facility, illustrates the scale of capital required even for a single demonstration-class unit — underscoring why factory economics, not reactor design, is the central determinant of whether the sector achieves cost competitiveness with conventional generation.

Licensing remains country-specific despite growing regulatory collaboration on safety standards.

In the United States, the Nuclear Regulatory Commission remains the primary commercial approval pathway, supported by Department of Energy cost-sharing and technical assistance. In the European Union, the newly adopted SMR Strategy proposes regulatory sandboxes and coordinated licensing to address the fact that existing frameworks were designed around conventional large reactors.

In India, nuclear licensing is itself subject to the pending Atomic Energy Act reforms, meaning regulatory clarity — not just construction capacity — remains a live variable for investors. This jurisdiction-by-jurisdiction approach means a developer's licensing progress in one market does not transfer to another, materially extending time-to-market for cross-border deployment strategies.

Fuel Supply

Many advanced small modular reactor designs require High-Assay Low-Enriched Uranium (HALEU), for which commercial supply is currently limited, according to both the International Atomic Energy Agency and the Observer Research Foundation. This fuel constraint applies disproportionately to next-generation designs such as sodium fast and high-temperature gas reactors — including TerraPower's Natrium and X-energy's Xe-100 — and represents a supply-chain risk independent of reactor licensing or construction progress.

Manufacturing Constraints

India's Central Electricity Authority, via the Observer Research Foundation, identifies the need to expand uranium supply, fuel fabrication capacity, manufacturing capability and skilled workforce as prerequisites for large-scale small modular reactor deployment domestically.

This mirrors a global pattern: heavy forgings, modular fabrication facilities and engineering, procurement and construction (EPC) capacity are not yet sized for the volume of projects implied by current government targets, including the European Union's projected 17–53 GW by 2050 and India's 100 GW by 2047.

Public Acceptance

Concerns over nuclear safety, waste management and land acquisition continue to affect project development timelines, per Observer Research Foundation analysis of India's nuclear expansion. While available data does not provide granular public-opinion metrics, the consistent appearance of public acceptance as a named constraint across institutional sources indicates it remains a live execution risk alongside the more frequently quantified capital, licensing and fuel-supply barriers.

Risk Category | Specific Constraint | Most Affected |

Financing | First-of-a-kind cost premium; ₹19 lakh crore India funding gap | All developers; India programme |

Regulatory | Country-specific licensing (NRC, European Commission); pending Indian legal reform | Cross-border deployment; India |

Fuel Supply | Limited commercial HALEU availability | Sodium fast & HTGR designs |

Supply Chain | Heavy forgings, EPC capacity, skilled workforce | Global, acute in India |

Public Acceptance | Safety perception, waste, land acquisition | India and emerging markets |

Risk Alert: India's regulatory transition requires detailed implementation rules under the amended Atomic Energy Act and Civil Liability for Nuclear Damage Act before private capital can accelerate at the scale the 100 GW target demands. This is currently the single largest near-term execution risk to India's SMR investment case — ahead of technology or fuel-supply risk.

Capital & Investment Implications

Are Small Modular Reactors commercially investable infrastructure assets?

Small modular reactors become commercially investable infrastructure assets once projects move beyond first-of-a-kind status into serial manufacturing, supported by confirmed government financing. The global market is estimated to reach US$300 billion by 2040, with capital opportunities spanning reactor developers, EPC contractors, fuel cycle infrastructure and grid integration — not reactor vendors alone.

Economics of SMRs

The capital economics of small modular reactors hinge on the relationship between CAPEX, OPEX and levelised cost of electricity (LCOE) across a manufacturing learning curve rather than a single project. TerraPower's approximately US$4 billion Natrium project for 345 MW of capacity represents a first-of-a-kind cost point; the central investment question for the sector is how steeply unit costs fall as fleet deployment scales — a trajectory the International Energy Agency ties to project delivery discipline and standardisation rather than design innovation.

Investment opportunity spans utilities, EPC contractors, fuel-cycle infrastructure and grid integration — not reactor vendors alone.

Utilities are procuring firm low-carbon capacity; EPC contractors are required to build out construction capacity at the scale implied by government targets; nuclear equipment and heavy forging suppliers face rising order volumes; and grid infrastructure providers such as Hitachi Energy — which partnered with Swedish developer Blykalla on 29 June 2026 specifically for grid integration — represent a distinct investment theme alongside fuel-cycle infrastructure addressing the HALEU supply constraint.

Government support is the dominant Small Modular Reactor financing model confirmed to date.

The United States' US$3.2 billion seven-year Advanced Reactor Demonstration Program, the United Kingdom's near-£600 million commitment to Rolls-Royce SMR, Sweden's first national nuclear financing package, and India's ₹20,000 crore Nuclear Energy Mission allocation are the four confirmed government-backed financing commitments underpinning current commercial activity. Export credit, sovereign funds and infrastructure funds are referenced in the broader investment framework but were not accompanied by specific verified transaction data in this report's research base.

India's Investment Opportunity

India's investment opportunity is defined by the scale gap between its 8.78 GW current capacity and 100 GW target, requiring an estimated ₹19 lakh crore — a sum the Observer Research Foundation states cannot realistically be met through public funding alone. The opening of nuclear generation to private participation, alongside controlled foreign investment structures under reform, is the regulatory precondition for this capital to mobilise.

Adani Group's confirmed target of 10 GW of nuclear capacity by 2035 through Adani Atomic Energy represents the most concrete private capital commitment in India's nuclear sector to date, alongside reported interest from NTPC, Reliance Industries, Tata Power and JSW Group.

Investment Watch: The global small modular reactor market is projected to reach US$300 billion by 2040. India alone requires an estimated ₹19 lakh crore of investment to reach its 100 GW target — a capital requirement larger than the country's nuclear sector has ever absorbed, and one that depends entirely on the pace of private-participation reform.

Future Scenarios & Forecast (2026–2035)

What is the outlook for Small Modular Reactors through 2035?

The outlook for small modular reactors through 2035 depends on whether construction-stage projects in the United States, Sweden and the United Kingdom deliver on schedule and cost, whether India's Atomic Energy Act and Civil Liability Act reforms are implemented with sufficient detail to unlock private capital, and whether HALEU fuel supply scales to meet next-generation design requirements. Three scenarios — accelerated, managed growth and delayed — bound the range of plausible outcomes.

Scenario 1: Accelerated Deployment

Under an accelerated scenario, the three United States Advanced Reactor Demonstration Program projects — TerraPower, X-energy and Kairos Power — complete construction on schedule and within reasonable cost tolerance, establishing a credible cost-reduction trajectory.

India's legal reforms are implemented with clear, investor-ready rules ahead of 2033, enabling private capital — including Adani Group's targeted 10 GW commitment — to mobilise rapidly. The European Union's 17–53 GW by 2050 projection tracks toward its upper bound as Sweden and the United Kingdom's Rolls-Royce SMR programmes proceed without major delay.

Scenario 2: Managed Growth

Under a managed growth scenario — the most consistent with currently verified data — United States construction projects proceed but with the cost and schedule variances typical of first-of-a-kind nuclear builds, moderating but not derailing investor confidence. India's reforms advance but implementation rules lag the 2033 indigenous deployment target, pushing meaningful private capital mobilisation toward the back half of the decade.

The European Union's SMR Strategy delivers steady but incremental progress toward its 2050 capacity range, and global market growth toward the US$300 billion by 2040 estimate proceeds unevenly across geographies.

Scenario 3: Delayed Commercialisation

Under a delayed scenario, first-of-a-kind cost overruns on flagship United States and European projects undermine confidence in the manufacturing learning-curve thesis, HALEU fuel supply constraints bind earlier than anticipated, and India's regulatory reform stalls without detailed implementation rules — keeping private capital on the sidelines and pushing the five SMRs by 2033 target toward slippage. Small modular reactors remain commercially viable in select government-backed markets (United States, Sweden, United Kingdom) but fail to achieve the broader fleet-scale cost reduction required for wider global adoption before 2035.

Licensing approvals, realised construction costs and India's implementation timeline are the indicators to monitor through 2035.

Investors and policymakers should track licensing approvals across the NRC and the European Commission; realised (not projected) cost outcomes on the TerraPower, X-energy and Kairos Power construction projects; AI data centre electricity demand growth as a commercial demand signal; HALEU fuel supply expansion; EPC and manufacturing capacity build-out; and the specific implementation timeline of India's Atomic Energy Act and Civil Liability for Nuclear Damage Act amendments.

GFJ Intelligence Note: India's five SMRs by 2033 target is the most time-bound, falsifiable commitment in this report. Its trajectory — more than any reactor design announcement — will indicate which of the three scenarios above is materialising for the Indian market specifically.

Strategic Recommendations

What should infrastructure decision-makers do now?

Infrastructure investors should prioritise developers with confirmed construction status and government cost-sharing; utilities and industrial companies should evaluate captive power and offtake structures; EPC contractors and technology developers should position for India's regulatory opening; and policymakers should accelerate implementation rules to convert legislative reform into investable certainty.

Infrastructure Investors should weight exposure toward developers with confirmed construction status and government cost-sharing — TerraPower, X-energy and Kairos Power in the United States, and Rolls-Royce SMR in Europe — over earlier-stage design announcements, given the wide gap between 68 active global designs and only 2 operating commercial plants.

Utilities should evaluate small modular reactors as a firm-capacity complement to renewables portfolios, monitoring realised cost outcomes from the current United States construction wave before committing to large-scale procurement.

Industrial Companies, particularly in steel, cement, aluminium and chemicals, should assess captive power and offtake structures, drawing on the precedent set by the construction-stage United States projects now under federal cost-sharing.

EPC Contractors should begin building modular fabrication and heavy-forging capacity ahead of demand, given that manufacturing constraints — not reactor design — are identified as a binding bottleneck across both global and India-specific verified data.

Technology Developers pursuing the Indian market should engage early with NPCIL and the Department of Atomic Energy, given the government's stated preference for combining indigenous designs (BSMR-200, SMR-55) with international technology partnerships.

Government & Policymakers, particularly in India, should prioritise rapid publication of detailed implementation rules under the amended Atomic Energy Act and Civil Liability for Nuclear Damage Act — the single most cited constraint on private capital mobilisation in verified research for this report.

India's Nuclear Ecosystem participants — including NTPC, Tata Power, Reliance Industries, JSW Group and Adani Group — should treat the 2033 indigenous SMR target and the 2047 capacity target as distinct milestones requiring different capital and partnership strategies.

Executive FAQ

What are Small Modular Reactors and why are they becoming commercially important?

Small modular reactors are factory-fabricated nuclear units, generally below 300 MWe, designed for modular construction and transport to site rather than bespoke on-site building. They offer firm, low-carbon electricity with lower upfront capital requirements than conventional large reactors, and rising demand from AI data centres and industrial decarbonisation has converted government interest into confirmed construction-stage financing in the United States, Sweden and the United Kingdom in 2026.

Which Small Modular Reactor companies are most likely to achieve commercial deployment before 2035?

TerraPower, X-energy and Kairos Power are the most advanced, having entered construction under United States Department of Energy cost-sharing on 23 June 2026. Rolls-Royce SMR has the strongest European financing backing, selected by Sweden and supported by close to £600 million in United Kingdom public funding. India's NPCIL targets five units by 2033, though this remains development-stage pending regulatory reform.

How do Small Modular Reactors compare economically with conventional nuclear power plants?

Small modular reactors aim to reduce construction risk through factory manufacturing rather than on-site bespoke building. First-of-a-kind projects — such as TerraPower's approximately US$4 billion Natrium facility — currently carry a cost premium that the International Energy Agency states will only fall as serial manufacturing scales. Direct, verified per-megawatt cost comparisons with conventional nuclear were not available in this report's research base.

What is India's strategy for developing Bharat Small Modular Reactors?

India's strategy combines the ₹20,000 crore Nuclear Energy Mission, indigenous reactor designs (BSMR-200, SMR-55), and legal reforms to the Atomic Energy Act and Civil Liability for Nuclear Damage Act intended to open the sector to private and foreign investment. The programme targets five operational SMRs by 2033 as a step toward 100 GW of total nuclear capacity by 2047.

Which industries will benefit most from Small Modular Reactors?

Steel, cement, aluminium, data centres, green hydrogen production and coal plant repowering are identified as the primary industrial beneficiaries, particularly in India's captive-power-oriented deployment model. AI data centres and district heating, as piloted by Finland's Steady Energy, are emerging global demand sources.

What regulatory reforms are still needed?

In India, detailed implementation rules under the amended Atomic Energy Act and Civil Liability for Nuclear Damage Act are required before private capital can mobilise at scale. Globally, the European Union's new SMR Strategy calls for regulatory sandboxes and coordinated licensing to address frameworks originally designed for conventional large reactors, while licensing remains country-specific between the United States and the European Union.

What should infrastructure investors monitor through 2035?

Investors should track realised construction costs and schedules on the TerraPower, X-energy and Kairos Power projects, the pace of India's Atomic Energy Act and Civil Liability Act implementation, HALEU fuel supply expansion, and progress against India's five SMRs by 2033 and the European Union's 17–53 GW by 2050 targets.

Legal Disclaimer

This report has been prepared by the Green Fuel Journal Research & Intelligence Team for general informational and strategic intelligence purposes only. It is based on publicly available data from sources verified as of the dates stated, including the International Energy Agency, International Atomic Energy Agency, European Commission, Government of India, Reuters and the Observer Research Foundation, among others cited in the References section below. Information in fast-evolving regulatory and project-development contexts, particularly relating to India's Nuclear Energy Mission and ongoing United States construction-stage projects, may change after publication.

This report does not constitute investment, legal, regulatory or financial advice and should not be relied upon as the sole basis for any investment or business decision. Green Fuel Journal makes no representation as to the completeness or continued accuracy of third-party data cited herein. Forward-looking statements, including scenario forecasts and capacity projections to 2035, 2040 and 2047, are based on currently available data and are inherently uncertain. Readers should consult qualified financial, legal and regulatory advisors before making investment decisions. All content is protected by copyright; reproduction without attribution to Green Fuel Journal is prohibited. For full terms, see greenfueljournal.com/disclaimers.

References & Strategic Sources

This report is backed by authoritative research, institutional analysis, industry intelligence, and strategic data sources.

International Organisations

International Energy Agency (IEA) — The Path to a New Era for Nuclear Energy (2025)URL: iea.org/reports/the-path-to-a-new-era-for-nuclear-energy

International Atomic Energy Agency (IAEA) — Small Modular Reactors (Updated 2025)URL: iaea.org/topics/small-modular-reactors

Government & Regulatory Publications

European Commission — Small Modular Reactors (Strategy Overview) (March 2026)URL: energy.ec.europa.eu/topics/nuclear-energy/small-modular-reactors_en

European Commission — EU Strategy for Small Modular Reactors (COM/2026/117) (10 March 2026)URL: energy.ec.europa.eu/news/commission-unveils-strategy

Press Information Bureau (Government of India) — Union Budget 2025–26: Nuclear Energy Mission (3 February 2025)URL: pib.gov.in/PressReleasePage.aspx?PRID=2099244

News Sources

Reuters — India Proposes Opening Nuclear Sector to Private Firms (1 February 2025)URL: reuters.com/world/india/india-budget...

Reuters — US Cost-Sharing Thrusts Next-Gen Nuclear into Construction Phase (23 June 2026)URL: reuters.com/business/energy/us-cost-sharing...

Reuters — Sweden Has Agreed First Financing Package for New Nuclear Reactors (25 June 2026)URL: reuters.com/business/energy/sweden-financing...

Reuters — Swedish Reactor Developer Blykalla Signs Cooperation Deal with Hitachi Energy (29 June 2026)URL: reuters.com/business/energy/blykalla-hitachi...

Reuters — Steady Energy Launches Pilot for Small Nuclear Heat Reactor in Finland (12 February 2026)URL: reuters.com/business/energy/steady-energy...

Reuters — India's Adani Aims to Build 10 GW Nuclear Power Capacity by 2035 (24 June 2026)URL: reuters.com/business/energy/adani-nuclear...

The Guardian — UK Financing Commitment to Rolls-Royce SMR (13 April 2026)URL: theguardian.com (full URL not captured in the research)

Research Institutions & Academic Sources

Observer Research Foundation Middle East (ORF Middle East) — Big Aspirations for Small Modular Reactors: Understanding India's Strategy on SMRs (24 April 2026)URL: orfme.org/research/big-aspirations-for-smrs

Manohar Parrikar Institute for Defence Studies and Analyses (MP-IDSA) — Small Modular Reactors and India: Institutional Drivers and Challenges (19 September 2025)URL: idsa.in/publisher/issuebrief/smrs-and-india

Closing Assessment

For infrastructure investors evaluating India SMR exposure specifically, the single highest-leverage action is to track the publication date of detailed implementation rules under the amended Atomic Energy Act and Civil Liability for Nuclear Damage Act — not reactor design progress.

Until those rules are published, the ₹19 lakh crore capital requirement behind India's 100 GW by 2047 target cannot mobilise at scale, regardless of how many private entrants, including Adani Group's confirmed 10 GW commitment, signal intent.

Investors should set a calendar trigger against this milestone rather than against India's five SMRs by 2033 target, which is a technology deployment marker, not a capital-deployment one.

Comments