Green Ammonia Exports 2027: Why India and China Are the Only Verified Leaders

- Green Fuel Journal

- 1 day ago

- 19 min read

GREEN FUEL JOURNAL — EXECUTIVE INTELLIGENCE REPORT

A comparative intelligence assessment of the two markets with confirmed export-grade momentum, and why the rest of the announced global pipeline remains unproven.

Green Fuel Journal Research & Intelligence Team — see our Editorial Standards and AI Usage Disclosure for how this report was produced and verified

A note on scope. This report covers only India and China — the two markets where Green Fuel Journal's research team was able to verify export-grade policy or commercial activity through named, dated, sourced material. Saudi Arabia, the UAE, Egypt, Oman, Morocco, the European Union, and North America are widely discussed as future green ammonia exporters, but as of this report's research cut-off, no verified project-level or policy-instrument data was available for these markets. We have chosen not to speculate on their positioning rather than fill the gap with unverified estimates. A follow-up report will assess these markets once comparable primary-source data is confirmed.

1. Executive Intelligence Synthesis

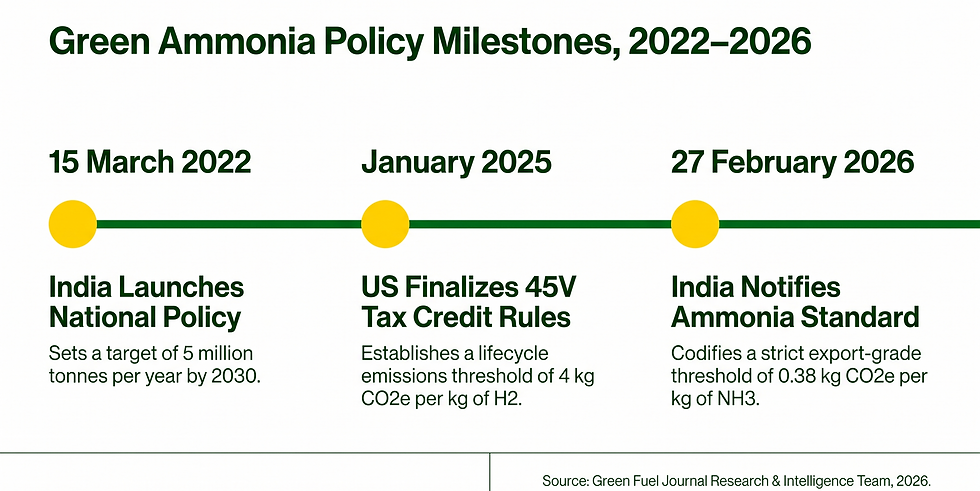

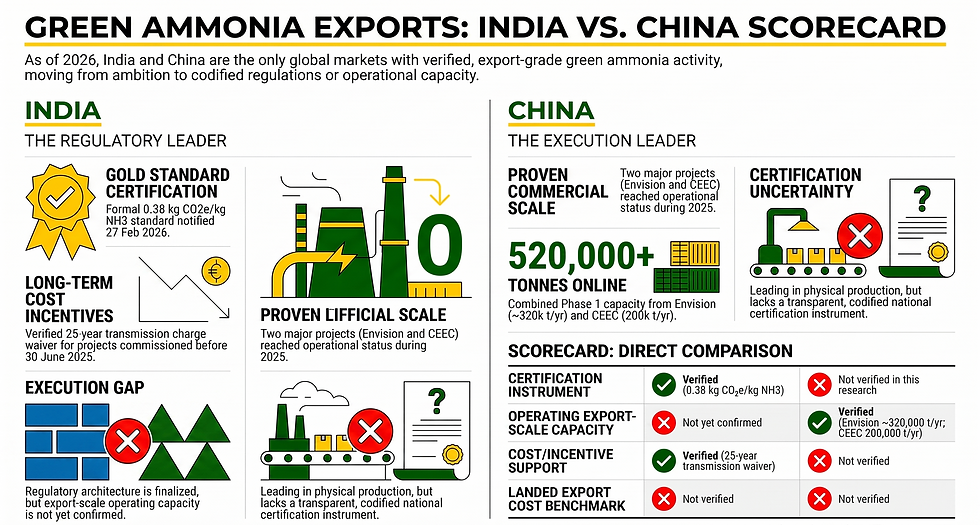

Direct Answer: As of 2026, only India and China have verified export-grade green ammonia activity. China leads on commercial-scale operation, with Envision Energy's Chifeng project and China Energy Engineering Corporation's (CEEC) Songyuan project both online or commencing operation in 2025. India leads on regulatory clarity, having notified a formal 0.38 kg CO₂e/kg NH₃ Green Ammonia Standard on 27 February 2026. Other widely discussed exporters — including Gulf states and Europe — remain at the announcement or policy-design stage with no verified commercial projects.

India notified a formal Green Ammonia Standard on 27 February 2026, setting a lifecycle emissions threshold of 0.38 kg CO₂e/kg NH₃ — the clearest single certification benchmark identified anywhere in this research. China's Envision Energy and CEEC moved green ammonia projects into operation during 2025, with CEEC's Songyuan facility alone backed by 800 MW of renewable capacity producing 200,000 tonnes/year in its first phase. No comparably verified project or certification instrument was identified for any other market in this research, narrowing the confirmed global field to these two countries for the 2026–2027 export window.

This does not mean other markets will not eventually compete. It means that, based on what can currently be confirmed, capital, policy attention, and buyer due diligence in 2026 and 2027 should be weighted toward the two markets that have moved from ambition to instrument and operation, rather than distributed evenly across an announced global field.

Five Executive Signals

Signal 1 — Verified leadership has narrowed to two countries.

FINDING: Of all markets reviewed, only India and China have named, dated, sourced evidence of export-grade green ammonia policy or commercial activity as of 2026.

SO WHAT: Investors and buyers currently treating the “global race” as a wide field are working from unverified assumptions about competitors that have not yet produced confirmable projects.

NOW WHAT: Near-term due diligence and capital screening should prioritise India and China first, with other markets tracked but not yet underwritten.

Signal 2 — China leads on commercial execution.

FINDING: Envision Energy's Chifeng project (Phase 1: 320,000 tonnes/year) and CEEC's Songyuan project (Phase 1: 200,000 tonnes/year, backed by 800 MW of renewables) both moved toward or into operation during 2025.

SO WHAT: China has demonstrated it can convert announced capacity into operating capacity within a defined timeframe — the single hardest test for any exporter.

NOW WHAT: Buyers seeking near-term supply should prioritise engagement with verified operating Chinese capacity over pre-FID projects elsewhere.

Signal 3 — India leads on certification clarity.

FINDING: India's Ministry of New and Renewable Energy notified a formal Green Ammonia Standard on 27 February 2026, defining green ammonia against a 0.38 kg CO₂e/kg NH₃ threshold averaged over the preceding 12 months.

SO WHAT: A codified national threshold gives international buyers and financiers a defined, auditable basis for classifying Indian-origin ammonia as “green,” reducing certification risk relative to markets without an equivalent instrument.

NOW WHAT: Offtake negotiators should treat India's standard as a template for contract-level certification language, even where the counterparty project is still pre-operational.

Signal 4 — Certification frameworks are diverging, not converging.

FINDING: India's 0.38 kg CO₂e/kg NH₃ ammonia threshold and the United States' 4 kg CO₂e/kg H₂ hydrogen threshold under the 45V tax credit rules (finalised January 2025) are structurally different accounting regimes measuring different molecules at different points in the value chain.

SO WHAT: Ammonia certified “green” under one jurisdiction's rules may not automatically satisfy a buyer operating under another jurisdiction's framework, creating friction in cross-border offtake contracts.

NOW WHAT: Buyers and sellers should specify the exact certification standard and measurement boundary in offtake contracts now, rather than assuming interoperability.

Signal 5 — The rest of the announced field remains unverified.

FINDING: No verified primary-source project or policy instrument was identified for the Gulf states, Europe, the UK, or North American ammonia-export capacity specifically, despite frequent public discussion of these regions as future exporters.

SO WHAT: Public market narratives about a crowded global export race currently outrun the confirmable evidence.

NOW WHAT: Treat announcements from unverified markets as pipeline to monitor, not capacity to underwrite, until primary-source project or policy documentation is available.

2. Macro Context: Why Green Ammonia, Why Now

Direct Answer: Green ammonia matters strategically because it functions as both a hydrogen carrier and a directly usable industrial commodity — as fertiliser feedstock and a candidate marine fuel — without the storage and transport penalties of pure hydrogen. 2025–2026 marks the point at which this shifted from a policy conversation to a measurable one, with India codifying a certification standard and China commissioning operating capacity in the same window.

Ammonia (NH₃) has been produced at industrial scale for over a century, almost entirely from fossil-derived hydrogen via the Haber–Bosch process. What has changed is the source of the hydrogen: green ammonia replaces fossil-derived hydrogen with hydrogen produced through renewable-powered electrolysis, and it inherits ammonia's existing advantage as a molecule that is far easier to store, ship, and handle than hydrogen gas itself.

This is why ammonia — rather than hydrogen directly — has become the preferred vehicle for internationally traded clean hydrogen value. Ammonia carries a substantial share of its mass as hydrogen, in a liquid form that can use existing global ammonia shipping, storage, and port infrastructure with modification rather than wholesale replacement.

Two developments in the 2025–2026 window turned this from a described opportunity into a measurable one.

First, the United States finalised its 45V clean hydrogen production tax credit rules in January 2025, setting a qualifying lifecycle threshold of 4 kg CO₂e per kg of hydrogen produced and introducing revised flexibility for electricity-matching and eligibility demonstration relative to the earlier draft rules. This is a domestic US production incentive rather than an export-market instrument, but it matters globally because it is one of the first fully finalised major-economy rulebooks for what counts as “clean” hydrogen — a reference point other jurisdictions' buyers and financiers will inevitably compare their own contracts against.

Second, and more directly relevant to export competitiveness, India notified its own Green Ammonia Standard on 27 February 2026, defining the emissions threshold specifically for ammonia rather than upstream hydrogen. This distinction matters for exporters: a standard written for the traded commodity itself, rather than an input several steps upstream, is more directly usable in an international offtake contract.

Meanwhile, project-level activity — the harder test of whether a market's ambitions convert into shippable tonnes — has so far been concentrated in China, where two large integrated projects moved from construction toward operation during 2025. This combination — India's regulatory instrument, China's operational capacity — is the basis for this report's central claim: as of 2026, the verified global race has two participants, not the wider field typically listed in industry commentary.

Readers tracking the policy side of this story in more depth may find Green Fuel Journal's coverage of India's National Green Hydrogen Mission a useful companion piece to this report.

3. India vs. China: Head-to-Head

Direct Answer: India and China lead the verified green ammonia export field on different axes. India has the clearer certification framework — a codified 0.38 kg CO₂e/kg NH₃ threshold and transmission-cost incentives. China has the clearer commercial execution — two large projects, from Envision Energy and CEEC, operating or commencing operation in 2025. Neither currently dominates on both dimensions simultaneously.

3.1 India: Regulatory Clarity, Execution Still Unproven at Export Scale

FINDING: India's Ministry of New and Renewable Energy (MNRE) notified the Green Ammonia Standard on 27 February 2026, setting the qualifying lifecycle emissions threshold at 0.38 kg CO₂e per kg NH₃, averaged over the preceding 12 months.

SO WHAT: This is the clearest single regulatory signal in the dataset — a specific, auditable, government-issued number that international buyers can reference directly in contracts.

NOW WHAT: Exporters and offtake partners should treat this standard as the current benchmark for India-origin certification claims.

India's standard sits on top of an earlier green hydrogen and ammonia policy framework that included priority grid connectivity and a 25-year waiver of inter-state transmission charges for qualifying projects commissioned before 30 June 2025. This waiver directly affects the delivered cost of power into electrolysis — the single largest input cost in green ammonia production — and therefore matters for export price competitiveness, even though this research did not surface a verified landed-cost figure to quantify the effect precisely.

What the current evidence does not establish is a verified, named Indian project operating at export scale comparable to China's Envision or CEEC facilities. India's demonstrated strength in this dataset is regulatory architecture; its demonstrated weakness is the absence of confirmed commercial-scale operating capacity to match. This is a meaningful gap for a report evaluating export readiness specifically: a standard without shipped tonnes is a necessary but not sufficient condition for export leadership.

3.2 China: Commercial Execution, Policy Instrument Less Transparent

FINDING: Two large Chinese projects have verifiably moved from construction into operation during 2025: Envision Energy's Chifeng zero-carbon hydrogen-ammonia project, and China Energy Engineering Corporation's (CEEC) Songyuan integrated hydrogen-ammonia-methanol complex.

SO WHAT: China has demonstrated the harder capability — converting announced capacity into operating capacity within a bounded timeframe, which is the primary point of failure for green ammonia projects globally.

NOW WHAT: Near-term supply-side due diligence should weight Chinese operating capacity more heavily than pre-FID capacity anywhere else in the dataset.

Reported figures for the Envision Chifeng project show some variation across sources — one dataset cites 320,000 tonnes/year for Phase 1 with a long-term target of 5 million tonnes/year, while a separate industry report from May 2025 cites 300,000 tonnes/year of capacity coming online that September. The direction and scale of the project are consistently confirmed, but the precise Phase 1 tonnage should be verified against Envision's own primary disclosure before being used in any financial model.

CEEC's Songyuan project is better specified in the current dataset: a first phase built around 800 MW of renewable generation capacity supporting 200,000 tonnes/year of green ammonia output, with expansion plans referenced toward 600,000 tonnes/year. Reporting places the first phase reaching or approaching operation around July 2025, with further expansion noted by December 2025.

What the current evidence does not establish for China is a specific, named national policy instrument — comparable to India's MNRE standard — governing certification or emissions thresholds for green ammonia exports. China's demonstrated strength in this dataset is commercial and industrial execution; its demonstrated weakness, at least in terms of what is publicly and verifiably documented in English-language and international sources, is the absence of an equivalently transparent certification framework. This does not mean no such framework exists — it means it was not independently confirmed, and should not be assumed either way.

3.3 Comparative Summary

Dimension | India | China |

Certification instrument | Verified — 0.38 kg CO₂e/kg NH₃, notified 27 Feb 2026 | Not independently confirmed |

Verified operating export-scale capacity | Not yet confirmed at comparable scale | Verified — Envision (~320,000 t/yr Phase 1) and CEEC (200,000 t/yr Phase 1) |

Cost/incentive support | Verified — 25-year transmission charge waiver for projects commissioned before 30 June 2025 | Not independently confirmed |

Landed export cost benchmark | Not verified | Not verified |

4. Operational Fundamentals: What Determines Export Competitiveness

Direct Answer: Export competitiveness in green ammonia depends on integrated performance across renewable power cost, electrolyser reliability, synthesis efficiency, certification, and export logistics — not any single input in isolation. Neither India nor China has disclosed a fully verified cost breakdown across this chain, which is itself a notable transparency gap in an otherwise fast-moving sector. Buyers and financiers currently have to underwrite each stage of the chain separately, using policy signals such as India's transmission waiver as a proxy for cost advantage rather than a confirmed delivered-cost figure.

Renewable electricity cost is the single largest driver of delivered ammonia cost, because electrolysis is energy-intensive and runs most economically against consistent, low-cost power. The production chain that determines this cost runs from renewable electricity, through electrolysis to produce green hydrogen, through Haber–Bosch synthesis to combine that hydrogen with nitrogen, into storage, and finally to export terminals for shipping. Each stage carries its own cost and reliability risk, and a project's export competitiveness is a function of how well these stages are integrated — not the strength of any one component alone.

Policy instruments like India's transmission charge waiver matter in principle by reducing the cost and risk of moving renewable power to the point of production, even though this report cannot currently quantify the effect in delivered-cost terms without a verified benchmark.

Certification and traceability add a second layer of complexity specific to green ammonia as a traded commodity rather than a domestically consumed one. A buyer in one jurisdiction needs assurance that ammonia certified “green” under an exporting country's rules will be recognised under the buyer's own regulatory or voluntary framework. As Signal 4 notes, India's ammonia-specific threshold and the United States' hydrogen-specific 45V threshold are not directly comparable instruments — they measure different molecules at different points in the chain. This is a foreseeable friction point for any offtake agreement that does not specify certification terms explicitly.

Export infrastructure — ports, ammonia storage tankage, and shipping capacity — is the stage of the chain with the least verified data for either India or China. Existing global ammonia shipping and port infrastructure provides a starting point, given that ammonia has been shipped internationally as a fertiliser feedstock commodity for decades, but the extent to which it requires modification for green-certified cargo, and whether India's or China's ports currently have sufficient dedicated capacity for scaled export, was not confirmed in this pass and should be treated as an open question.

5. Named Company and Project Case Studies

Direct Answer: The clearest verified examples of green ammonia projects moving from announcement to operation are China's Envision Energy Chifeng project and CEEC's Songyuan project, both progressing through 2025. India's leading case is not a single named project but its national policy pipeline, anchored by the MNRE Green Ammonia Standard notified in February 2026. No named Indian project of comparable operating scale to the two Chinese examples was identified in this research, making China the stronger source of verified near-term supply and India the stronger source of verified certification credibility.

5.1 Envision Energy — Chifeng Zero-Carbon Hydrogen-Ammonia Project (China)

Envision Energy's Chifeng project is one of the clearest examples in this dataset of a green ammonia project crossing from announcement into commercial-scale operation. Phase 1 capacity is reported at 320,000 tonnes per year in one source (with a competing industry report from May 2025 citing 300,000 tonnes/year coming online that September, against a stated long-term target of 5 million tonnes per year.

Phase 1 came online during 2025, with further expansion under development. The scale of the long-term target, if realised, would represent a materially significant share of any future global green ammonia trade — though it should be treated as a target rather than a confirmed trajectory until later phases are independently verified.

5.2 China Energy Engineering Corporation (CEEC) — Songyuan Integrated Project (China)

CEEC's Songyuan project integrates green hydrogen, ammonia, and methanol production at a single site — a design choice that spreads project risk across multiple offtake markets rather than depending on ammonia exports alone. The first phase is built around 800 MW of renewable generation capacity and 200,000 tonnes/year of ammonia output, reaching or approaching operation around July 2025, with expansion toward 600,000 tonnes/year referenced in reporting through December 2025. This project is, on the currently available evidence, the most fully specified operating green ammonia asset in either market covered by this report.

5.3 India's Policy-Backed Pipeline

India's leading entry in this section is not a single company or project but the regulatory architecture itself — the MNRE Green Ammonia Standard (0.38 kg CO₂e/kg NH₃, notified 27 February 2026) combined with the earlier transmission-cost incentive structure. This report was not able to verify a named Indian green ammonia project operating at a scale comparable to Envision or CEEC.

Readers evaluating India-specific opportunities should treat the country's current position as “policy-ready, execution-unproven at export scale” until a comparable named, operating project is independently confirmed.

For readers tracking specific Indian project announcements as they reach financial close, Green Fuel Journal's ongoing India green hydrogen coverage will be updated as verified data becomes available.

6. Friction, Risk and Systemic Bottlenecks

Direct Answer: The principal risks to the green ammonia export market are certification fragmentation between jurisdictions, an unverified gap between announced and operating capacity globally, and the absence of confirmed cost or logistics benchmarks even in the two leading markets. Beyond India and China, the announced global project pipeline remains substantially unproven. These risks compound: a buyer facing both an unresolved certification question and an unverified delivery timeline carries meaningfully more contract risk than either issue alone would suggest, which is why offtake terms should address both explicitly.

6.1 Certification Fragmentation

India's ammonia-specific 0.38 kg CO₂e/kg NH₃ threshold and the United States' hydrogen-specific 4 kg CO₂e/kg H₂ threshold under 45V are two different accounting regimes, measuring different points in the value chain, finalised roughly a year apart (January 2025 and February 2026 respectively).

Neither this report nor the underlying research identified a confirmed interoperability agreement between these — or any other — national standards. Every cross-border offtake contract currently carries the risk that “green” as certified by the seller's jurisdiction will not automatically satisfy the buyer's jurisdiction or corporate procurement policy.

6.2 The Announcement-to-Operation Gap

The proportion of the announced global green ammonia pipeline likely to reach financial investment decision or operation by 2027 could not be verified from primary sources in this research. Industry commentary broadly discusses a large global pipeline of announced projects, but China's Envision and CEEC projects are the clearest counter-examples in this dataset — announced projects that did convert to operation within a defined window. They should be read as evidence that conversion is possible, not as evidence of the conversion rate across the broader announced pipeline.

6.3 Absence of Verified Cost Benchmarks

No verified levelised cost of ammonia (LCOA), levelised cost of hydrogen (LCOH), capital expenditure, or landed-cost-to-destination-market figure was identified for either India or China, despite these being the metrics that would most directly support an investment ranking. This is a material limitation for any reader using this report for capital allocation decisions, and it is the primary reason this report ranks markets on verified activity rather than on cost competitiveness.

6.4 Where the Rest of the World Stands

No verified named project or specific governing policy instrument for green ammonia exports was identified in this research for the Gulf states, the European Union, the United Kingdom, or North America — markets frequently discussed in industry commentary as future exporters. This is presented as a finding, not a limitation of this report's scope: it indicates that, as of the current research window, public discussion of a wide multi-country export race is running ahead of the confirmable evidence. Readers with existing exposure to announcements from these markets should treat them as pipeline to monitor rather than capacity to underwrite until comparable primary-source verification exists.

7. Capital and Investment Implications

Direct Answer: Near-term capital allocation in green ammonia should weight verified operating capacity in China and verified regulatory clarity in India more heavily than announced projects elsewhere. Without verified cost benchmarks, this report does not rank specific return potential — it ranks confidence in execution.

That distinction matters for investors: an unranked list of verified facts is more useful, and more defensible, than a precise-looking return estimate built on unverified inputs. Capital directed outside India and China should be treated as policy and announcement risk rather than execution risk.

Absent verified cost, financing, or landed-price data, this report does not attempt to produce a ranked risk-return matrix — doing so would require inputs this research could not confirm, and a fabricated ranking would be worse than no ranking at all. What can be responsibly said is narrower but still actionable.

China currently offers the strongest evidence base for near-term supply exposure, given two verified projects with disclosed capacity figures moving into operation during 2025. Diligence on Chinese counterparties should focus on securing primary disclosure to resolve the Envision Chifeng tonnage discrepancy noted in Section 5.1, and on independently verifying the certification basis under which any exported ammonia would be sold, given the absence of a confirmed Chinese national green ammonia standard in this research.

India currently offers the stronger regulatory foundation for structuring future offtake agreements, given its codified 0.38 kg CO₂e/kg NH₃ standard. Investors and buyers engaging with India-based projects should treat the standard as a credible certification anchor while separately underwriting each individual project's execution risk, since this report did not identify a named Indian project with verified operating capacity comparable to the Chinese examples above.

Capital directed toward markets outside India and China — where this report found no verified project or policy instrument — should be treated as exposure to policy and announcement risk specifically, distinct from the execution risk that applies even within the two verified markets.

8. Future Scenarios (2026–2035)

Direct Answer: Three plausible pathways shape the green ammonia market through 2035: continued India–China dual leadership with slow entry from other markets; China consolidating a durable first-mover advantage while other markets stall at the policy stage; or a broader field emerging only once verified cost and certification interoperability issues are resolved. These are presented as analytical scenarios, not forecasts, given the absence of verified market-sizing data.

Scenario 1 — Dual Leadership, Gradual Broadening

India and China remain the two most active markets through the late 2020s, with China's operating capacity continuing to scale from the Envision and CEEC base, and India converting its regulatory head start into named, verified operating projects. Other markets gradually produce verifiable projects and policy instruments, broadening the field by the early 2030s without displacing the two current leaders.

Scenario 2 — China Consolidates a First-Mover Advantage

China's demonstrated ability to convert announced capacity into operating capacity compounds: earlier operation means earlier offtake relationships, earlier operational learning, and earlier cost reduction. India's regulatory clarity does not translate into comparable operating scale quickly enough to prevent China from becoming the default reference supplier for buyers seeking near-term volume, even where India offers a cleaner certification story.

Scenario 3 — Certification Fragmentation Slows Everyone

The divergence between national certification frameworks — illustrated by the India-US comparison in Section 6.1 — becomes a genuine trade barrier rather than a manageable contract detail. Buyers hesitate to commit to long-term offtake without an interoperable international standard, slowing capital deployment across all markets, including India and China, until a harmonisation mechanism emerges.

9. Strategic Recommendations

Direct Answer: Investors, developers, policymakers, and industrial buyers should act on verified evidence rather than announced ambition before 2027.

Investors should weight diligence toward China's two operating projects and India's codified standard. Developers should treat certification and disclosure as commercial assets.

Policymakers outside India and China should prioritise publishing a named, dated certification instrument comparable to India's February 2026 notification.

Industrial buyers should specify certification terms explicitly in every offtake contract rather than assuming green labels are portable across jurisdictions.

For Investors

Prioritise diligence on China's verified operating projects and India's regulatory framework over announced-only projects in unverified markets. Commission independent verification of the Envision Chifeng Phase 1 tonnage discrepancy before using it in any financial model. Do not rely on this or any current public report for a cost-based ranking until verified LCOA/LCOH data becomes available.

For Developers

India-based developers should use the MNRE standard as a marketing and contracting asset immediately — it is a genuine differentiator relative to markets without an equivalent instrument. China-based developers should prioritise disclosure of a clear certification methodology, given the current absence of a verified national standard in international-facing documentation.

For Policymakers

Markets outside India and China seeking export credibility should prioritise publishing a named, dated, primary-source certification instrument — India's February 2026 notification is a directly usable template. Bilateral or multilateral work toward certification interoperability, particularly between India-style ammonia-specific thresholds and hydrogen-specific thresholds like the US 45V framework, would materially reduce the friction identified in Section 6.1.

For Industrial Buyers

Specify the exact certification standard and measurement boundary in every green ammonia offtake contract rather than assuming “green” is a portable label across jurisdictions. Treat verified operating capacity — currently limited to the Chinese projects identified in this report — as the basis for near-term procurement planning.

Bottom line for the primary reader: Until a third market produces evidence of comparable weight — a named operating project or a codified national standard — treat India and China as the only two green ammonia export markets worth underwriting today, and revisit that position only when new primary-source data justifies it.

10. Executive FAQ

Which countries currently lead verified green ammonia exports?

India and China are the only two markets with verified, named, dated evidence of export-grade green ammonia policy or commercial activity as of 2026. China leads on operating commercial-scale capacity; India leads on codified certification. No other market currently has comparable verified project or policy documentation.

Is India likely to become a major green ammonia exporter?

India has the clearest regulatory foundation of any market assessed in this report, anchored by the 0.38 kg CO₂e/kg NH₃ Green Ammonia Standard notified on 27 February 2026 and an earlier 25-year transmission charge waiver for qualifying projects. Execution is the open question: no Indian project has yet reached the operating scale China's Envision and CEEC facilities have demonstrated.

What are the biggest risks in the green ammonia export market today?

The most significant verified risks are certification fragmentation between national frameworks, an unquantified gap between announced and operating global capacity, and the absence of verified cost benchmarks even in the two leading markets. These risks apply within India and China as well as to markets outside them.

Are Gulf states or Europe currently competitive in green ammonia exports?

No. This report's research did not identify a verified, named project or governing policy instrument for green ammonia exports in the Gulf states, the European Union, the UK, or North America. This does not rule out future competitiveness, but current public discussion of these markets as active exporters is not yet supported by confirmable primary-source evidence.

Which companies are leading verified green ammonia project execution?

Envision Energy and China Energy Engineering Corporation (CEEC) are the two companies with verified, named, dated evidence of green ammonia projects moving into operation, both in China during 2025. No comparably verified named commercial project was identified in India.

Can green ammonia certified in one country be sold as “green” in another?

Not automatically. India's ammonia-specific 0.38 kg CO₂e/kg NH₃ threshold and the United States' hydrogen-specific 4 kg CO₂e/kg H₂ threshold under 45V are structurally different accounting regimes. Buyers and sellers should specify the applicable certification standard explicitly in offtake contracts rather than assuming interoperability.

11. Legal Disclaimer

This report is published by Green Fuel Journal for informational and educational purposes only. It does not constitute investment, legal, tax, or financial advice, and should not be relied upon as the sole basis for any investment or business decision. This report is based on the best available information at the time of research and explicitly identifies areas where verified primary-source data was not available; readers should conduct independent due diligence before acting on any information contained here. Forward-looking statements, including the scenarios in Section 8, are analytical projections, not forecasts or guarantees of future outcomes.

Full disclaimer terms are available at greenfueljournal.com/disclaimers.

References & Strategic Sources:

This report is backed by authoritative research, institutional analysis, industry intelligence, and strategic data sources.

Ministry of New and Renewable Energy (MNRE) published the Green Ammonia Standard for India on 27 February 2026, establishing India's official framework for defining and certifying green ammonia. This marked a significant milestone in strengthening the country's low-carbon ammonia ecosystem and export competitiveness.Source: https://mnre.gov.in/en/green-ammonia-standard/

Press Information Bureau (PIB), Government of India issued a press release on the Green Ammonia and Green Methanol Standards on 7 March 2026, outlining the new emission thresholds and certification framework under the National Green Hydrogen Mission.Source: https://pib.gov.in/PressReleasePage.aspx?PRID=2236255

Government of India policy coverage announced the Green Hydrogen and Green Ammonia Policy on 15 March 2022, targeting 5 million tonnes of green hydrogen production annually by 2030 while introducing measures such as transmission charge waivers, priority grid connectivity, and support for export-oriented projects.Source: https://www.thehindubusinessline.com/economy/policy/govt-notifies-green-hydrogen-green-ammonia-policy/article65223953.ece

US Treasury and Internal Revenue Service (IRS) released the final tax credit rules for clean hydrogen production (Section 45V) on 14 January 2025, providing greater regulatory certainty for clean hydrogen and green ammonia investments in the United States.Source: https://www.ammoniaenergy.org/articles/final-tax-credit-rules-for-clean-hydrogen-production-in-the-us-released/

US Treasury and IRS subsequently published the Final Hydrogen Production Tax Credit Regulations on 23 January 2025, clarifying implementation details and eligibility requirements for the Section 45V tax credit.Source: https://www.wsgr.com/en/insights/treasury-and-irs-release-final-hydrogen-production-tax-credit-regulations.html

Industry project coverage reported that Energy China plans to bring 200,000 tonnes of renewable ammonia production capacity online in September 2025, marking one of China's largest commercial renewable ammonia developments.Source: https://www.ammoniaenergy.org/articles/energy-china-200000-tons-of-renewable-ammonia-capacity-online-this-september/

Industry project coverage also reported that Envision Energy expects to commission 300,000 tonnes of renewable ammonia production capacity in September 2025, reinforcing China's ambition to become a major renewable ammonia producer.Source: https://www.ammoniaenergy.org/articles/envision-300000-tons-of-renewable-ammonia-capacity-online-this-september/

An industry report published on 7 July 2024 examined how renewable ammonia is progressing in China, highlighting policy developments, project investments, and accelerating commercialization of green hydrogen-derived fuels.Source: https://www.ammoniaenergy.org/articles/renewable-ammonia-progresses-in-china/

Additional industry coverage, dated 25 December 2025, reported that China's green ammonia sector had entered commercial operation, signalling the transition from demonstration projects to commercial-scale deployment.Source: https://www.ammoniaenergy.org/articles/chinas-green-ammonia-sector-enters-commercial-operation/

© 2026 GreenFuelJournal.com · Strategic Intelligence for the Global Energy Transition

Comments